100% FDI in Insurance: Breaking Down the Sabka Bima Sabki Raksha Act

India's insurance sector has just undergone its most significant structural reform since the original IRDAI Act of 1999. The Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act, 2025, passed by Parliament on 17 December 2025, raises the FDI limit in Indian insurance companies to 100% of paid-up equity capital under the automatic route.

The FDI headline has dominated coverage. But full foreign ownership is only one of several provisions, each with distinct implications for insurers, reinsurers, intermediaries, and consumers. This article breaks down what has changed and what it means for the sector.

Background: Why This Reform, Why Now

India's insurance penetration stands at approximately 4.2% of GDP, against a global average of 7%. The government's stated goal, Insurance for All by 2047, requires substantially higher coverage across health, life, and general insurance. The prior 74% cap was seen by global insurers as a structural barrier to long-term capital deployment. Swiss Re estimates average annual premium growth of 6.9% in India between 2026 and 2030, outpacing most major markets. This reform is an attempt to attract the capital needed to realise that potential.

What the Act Actually Changes

The Act amends three statutes: the Insurance Act, 1938; the Life Insurance Corporation Act, 1956; and the IRDAI Act, 1999. Changes span ownership, capital thresholds, intermediary regulation, enforcement, and governance.

1. Foreign Ownership

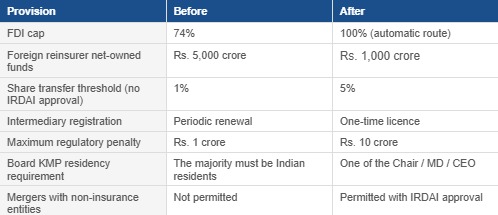

Foreign investors may now hold up to 100% of paid-up equity capital under the automatic route.

- Conditions remain at the central government's discretion.

- Foreign Investment Rules aligned on 30 December 2025.

- IRDAI's Registration Regulations still reference the 74% cap pending amendment. Verify with legal counsel before restructuring.

2. Capital Requirements for Reinsurers

Minimum net-owned funds for foreign reinsurers cut from Rs. 5,000 crore to Rs. 1,000 crore.

- Directly lowers the entry barrier for global reinsurers.

- Especially significant for GIFT City's IFSC, a key government focus for reinsurance capacity.

- Global reinsurers that previously found the threshold prohibitive are expected to reassess India strategies.

3. Share Transfers and M&A

- Share transfer threshold not requiring prior IRDAI approval raised from 1% to 5%.

- Approval still required if a single transferee's holding would cross 5%.

- Reduces friction in secondary transactions and simplifies M&A structures.

- May accelerate consolidation in a sector where deal activity has historically been slow.

4. Intermediary Registration and Recognition

- One-time licensing replaces periodic renewal for all intermediaries.

- MGAs and insurance repositories formally recognised as intermediaries for the first time.

- MGAs can perform: underwriting, policy issuance, premium collection, claims payment, and reinsurance negotiation.

- Recognition brings full IRDAI registration requirements and regulatory obligations.

- Recognised intermediaries: brokers, corporate agents, TPAs, MGAs, and insurance repositories.

5. Enforcement: Penalties and Disgorgement

- Maximum penalties raised tenfold: Rs. 1 crore to Rs. 10 crore, now covering intermediaries explicitly.

- Mis-selling complaints against life insurers rose 14% in FY25 a direct catalyst for this change.

- IRDAI granted disgorgement powers to recover wrongful gains from mis-selling and commission violations.

- Applies across insurers and intermediaries no carve-outs.

6. Board Composition

- Previous rule: majority of board and KMPs must be resident Indian citizens.

- New rule: only one of the Chairperson, MD, or CEO must be a resident Indian citizen.

- Foreign groups now have far greater flexibility in structuring leadership and integrating Indian operations globally.

- For those weighing a full buyout, this governance change may matter as much as the ownership cap.

7. Corporate Restructuring

- New statutory framework allows mergers between insurance companies and non-insurance entities, subject to IRDAI approval.

- Previously not permitted under any framework.

- Opens the door to new ownership models blending insurance with adjacent financial services.

Implications for the Sector

- Existing joint ventures: Partnerships will not dissolve, but the dynamic shifts. Indian partners once required by regulation must now justify their value commercially.

- New foreign entrants: Full ownership is structurally possible. Speed of entry depends on regulatory alignment and the complexity of building underwriting capacity in India.

- Intermediaries: One-time licensing eases entry. But tenfold penalties and disgorgement powers make non-compliance significantly more costly. Wider access, higher accountability.

- Consumers: More competition and stronger enforcement should translate into better products and fairer pricing, particularly in underpenetrated segments.

A Note on Regulatory Alignment

IRDAI's Registration Regulations of 2024 were structured around the previous 74% cap and are pending amendment. Companies restructuring their shareholding should verify the applicable regulatory position with legal counsel before proceeding.

Key Changes at a Glance

Symbo's View

The Sabka Bima Sabki Raksha Act signals a clear regulatory intent: open the market wide, but hold every participant to a higher standard. For embedded insurance platforms, this is a structural opportunity. Global insurers entering with full ownership will seek proven, API-first distribution infrastructure rather than build from scratch. Stronger enforcement means the compliance layer is no longer optional it is a competitive differentiator. The market is about to become larger and more demanding at the same time.

Unlock Whitepaper

A structured deep dive combining industry insights, on-ground learnings, and proven models curated by domain experts.

Stay Ahead of Insurance Innovation

Get monthly insights on regulations, product trends, technology shifts, and Symbo updates that shape the future of insurance.