India Has 12 Million Gig Workers. Almost None Have Insurance.

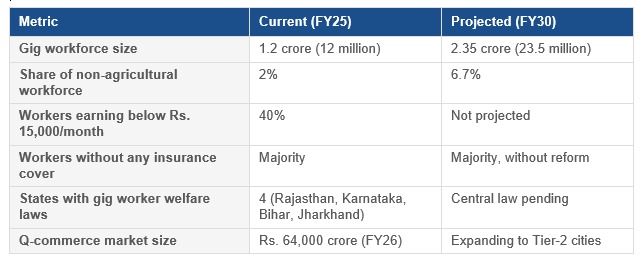

India's gig workforce grew from 7.7 million in FY21 to 12million in FY25, projected to reach 23.5 million by 2030. It powers fooddelivery, quick commerce, and last-mile logistics at a scale no otheremployment category has matched. Yet the Economic Survey 2025-26 documentedwhat the growth numbers obscure: the near-total absence of a financial safetynet for the workers behind it.

No provident fund. No ESI. No gratuity. For most gig workers,no insurance of any kind. This is not a fringe issue. It is a structural gap ina workforce contributing an estimated Rs. 2.35 lakh crore to GDP, and theregulatory response is now actively closing in.

The Numbers Behind the Gap

Why Traditional Insurance Products Fail This Segment

• Variable income, fixed premiums: Gig workersearn Rs. 200-600 a day depending on demand. Annual or monthly premiumstructures built for salaried income simply do not hold.

• No employer link, no group cover: Classified asindependent contractors, gig workers fall outside employer-linked group schemesentirely.

• Distribution does not reach them: Agent networksand bank branches barely penetrate this segment. The only channel with realreach is the platform itself.

What the Regulatory Framework Now Requires

• Social Security Code, 2020: Gig workers areformally recognised outside the employer-employee framework. Aggregators mustcontribute 1- 2% of annual turnover into a Social Security Fund, covering lifeinsurance, health, and pension benefits.

• 90-day eligibility rule (draft, January 2026): Workersmust be engaged for 90 days in a year to qualify for central benefits, risingto 120 days across multiple aggregators.

• State welfare laws now live in four states: Rajasthan(2023), Karnataka (2025), Bihar and Jharkhand (2025) all mandate platformlevies, worker registration, and welfare boards. Karnataka's law is the mostdetailed and likely the national template.

• PM-JAY access via e-Shram: Union Budget 2025-26extended PM-JAY health cover of Rs. 5 lakh per family to gig workers registeredon e-Shram. Over 31.2 crore workers are registered. Active utilisation remainsthe challenge.

What the Regulatory Framework Now Requires

• Social Security Code, 2020: Gig workers areformally recognised outside the employer-employee framework. Aggregators mustcontribute 1- 2% of annual turnover into a Social Security Fund, covering lifeinsurance, health, and pension benefits.

• 90-day eligibility rule (draft, January 2026): Workersmust be engaged for 90 days in a year to qualify for central benefits, risingto 120 days across multiple aggregators.

• State welfare laws now live in four states: Rajasthan(2023), Karnataka (2025), Bihar and Jharkhand (2025) all mandate platformlevies, worker registration, and welfare boards. Karnataka's law is the mostdetailed and likely the national template.

• PM-JAY access via e-Shram: Union Budget 2025-26extended PM-JAY health cover of Rs. 5 lakh per family to gig workers registeredon e-Shram. Over 31.2 crore workers are registered. Active utilisation remainsthe challenge.

What Products actually works for this segment.

• Usage-linked premiums: Per-delivery, per-trip,or per-active-day pricing. Fixed monthly premiums do not work for variableincome; coverage that scales with earnings does.

• Accident cover first: A delivery worker on theroad 10-12 hours a day in urban traffic faces real occupational risk. Incomeloss from a minor accident can be devastating at Rs. 15,000/month.

• Platform-embedded enrolment: One-step sign-upthrough the worker dashboard, premium deducted from existing payment flows.Standalone insurance applications in this segment will see near-zeroconversion.

• Fast digital claims: A worker who cannot workdue to injury cannot wait weeks for a claim. Settlement in 24-48 hours is the benchmark that makes the product credible.

TheQuick Commerce Factor

India's quick commerce market hit Rs. 64,000 crore in FY26. An estimated20 lakh new gig jobs are expected in 2026 as Blinkit and Zepto expand intoTier-2 cities. Every new worker added to this ecosystem is, today, unprotected.The faster quick commerce grows, the wider the gap

What Platforms Should Be Doing Now

• Audit your state exposure: Welfare levy andregistration obligations are live in Rajasthan, Karnataka, Bihar, andJharkhand. Central rules follow. Do not wait.

• Model the fund contribution: 1-2% of annualturnover is material at scale. Build the liability into your financial modelbefore the rules are notified.

• Enrol at onboarding, not after: Attach rates arehighest when a worker first activates. Retrofitting insurance into an existingrelationship is significantly harder.

• Use your data: Earnings, trip frequency, andactive hours are already collected. An API integration with an embedded insurerconverts that into real-time, usage-based underwriting instantly.

Symbo's View

The gig worker insurance gap is large,well-documented, and now regulatory. Four states have legislated. Central rulesare in draft. The Economic Survey has named it as a priority. What has beenmissing is not awareness but the product and distribution infrastructure toclose it at the right price point. Embedded insurance, built on usage-basedpricing and platform-linked distribution, is that infrastructure. The questionfor platforms is no longer whether to act. It is how fast.

Unlock Whitepaper

A structured deep dive combining industry insights, on-ground learnings, and proven models curated by domain experts.

Stay Ahead of Insurance Innovation

Get monthly insights on regulations, product trends, technology shifts, and Symbo updates that shape the future of insurance.